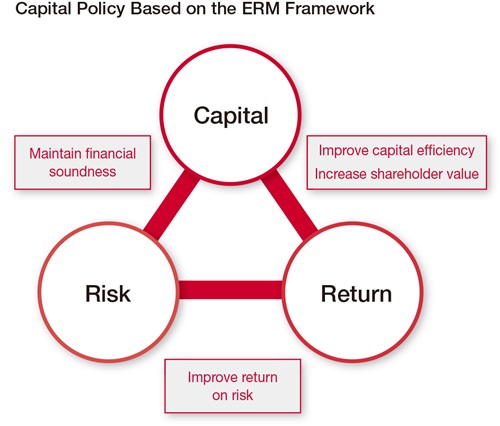

Based on our Strategic Risk Management (ERM)* framework, we aim to provide attractive shareholder returns and maximize corporate value based on a balance between profit and capital.

- ERM:Enterprise Risk Management

Shinji Tsuji

Group CFO

Representative Director,

Deputy President and

Senior Managing Executive Officer

Basic Capital Policy

The basic capital policy of the Sompo Holdings Group entails appropriately controlling the balance between profit, capital, and risk and maintaining robust financial soundness based on the Strategic Risk Management (ERM) framework. We thereby aim to achieve growth that will put our profit levels within the global top 10 insurers, which is our vision for the growth of the Group; steadily improve capital efficiency to realize adjusted consolidated ROE of 10.0% or more; and provide attractive shareholder returns (shareholder dividends and share buybacks) commensurate with our profit and capital levels.

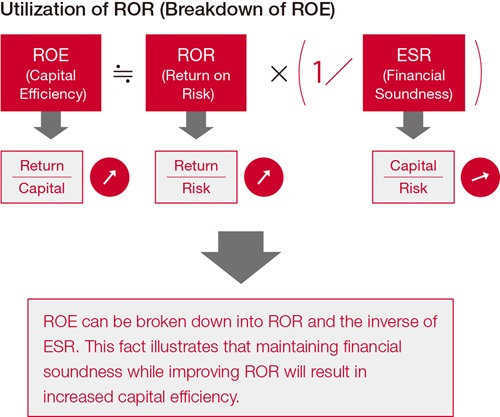

Based on our basic capital policy, we apply management procedures for financial soundness based on the European Union’s Solvency II and other international capital regulations and utilize return on risk (ROR) as an indicator for making management decisions in a wide range of fields, including performance evaluation and investment. We also strive to enhance capital quality on a continuous basis and to promote capital policy that facilitates the acquisition of returns in order to maximize corporate value.

Improvement of Capital Efficiency

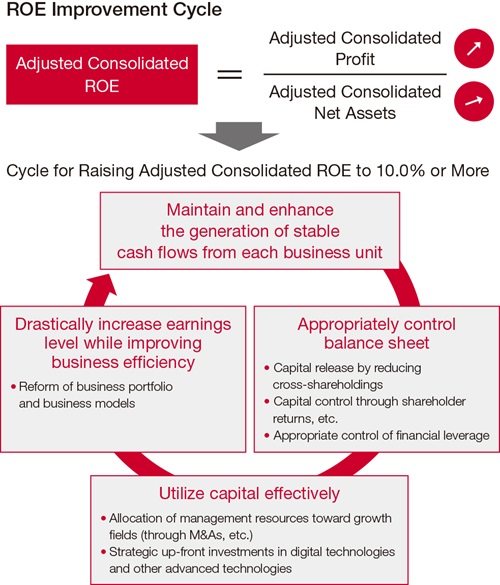

By implementing an operating cycle for improving capital efficiency (ROE) sustainably that was established on the basis of its Strategic Risk Management framework, the Group appropriately controls its balance sheet through such measures as continuing to reduce its cross-shareholdings, increasing shareholder returns, and managing financial leverage while enhancing its systems for generating stable cash flows in each of its businesses. On this basis, we will allocate management resources toward growth fields (through M&As, for example) and conduct forward-looking strategic investments in various fields with the potential to bring about new businesses and to revolutionize industry structures, such as digital technologies and advanced sciences and technologies. In addition, we will work to achieve drastic improvements in business efficiency and profit levels by transforming our business portfolio and business models. As a result, we intend to achieve sustainable growth in adjusted consolidated profit and adjusted consolidated ROE and reach our medium-tolong- term targets.

Policy on Cross-Shareholdings

The Company’s subsidiary Sompo Japan Nipponkoa Insurance Inc. engages in cross-shareholdings for the purposes of receiving investment returns in the form of dividend income and share price appreciation, enhancing relations with the insurance sales channels and business partners, and maintaining and strengthening insurance transactions with corporate clients.

The Board of Directors annually examines the rationale for continuing to maintain cross-shareholding accounts. These examinations consider the future use of the shares based on the cross-shareholding objectives, such as supporting insurance transactions and strengthening alliances, review the long-term outlooks for unrealized gains from value appreciation and the share value, and set quantitative risk and return assessment benchmarks for the associated insurance transactions and share values.

As part of the Group’s capital policy, the Company implements a management policy of allocating a portion of the gains generated from the continuous selling of crossshareholdings to growth business investments, such as overseas M&A activities, to support the maintenance of financial soundness and improve capital efficiency. These activities are conducted in accordance with the mid-term and annual retention and disposal plans for cross-shareholdings established by the Board of Directors.

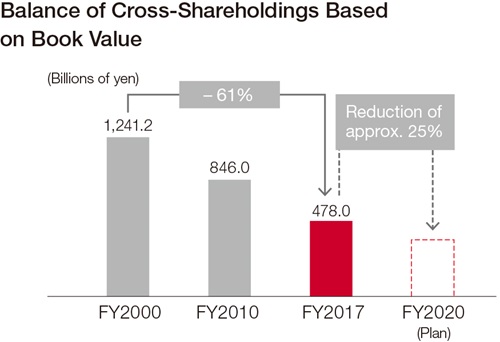

Under the current Mid-Term Management Plan, we plan to reduce cross-shareholdings by around ¥100.0 billion per year. The amount of reduction in fiscal 2017 was ¥109.6 billion. We will continue to reduce the overall balance of crossshareholdings going forward based on quantitative evaluations and extensive discussions with counterparties.

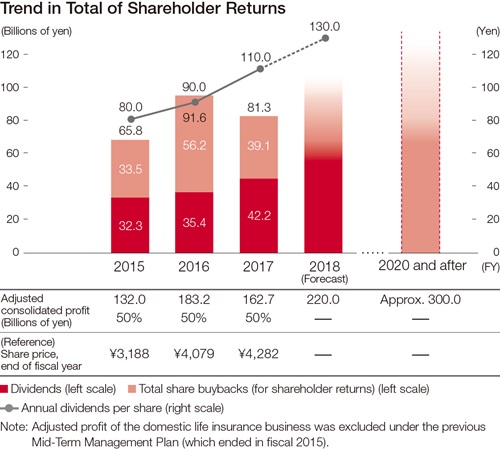

Shareholder Returns

Sompo Holdings’ basic policy is to issue stable dividends based on evaluations of the Company’s financial position and the outlook for the operating environment and with a view to increasing dividends in line with profit growth. We also consider flexible share buybacks as a potential option when deemed appropriate based on the Company’s stock price and capital condition. Through this approach, we seek to provide attractive shareholder returns.

Based on growth in adjusted consolidated profit, we plan to proactively increase the total of shareholder returns (total dividend payments + total share buybacks). In the Mid-Term Management Plan, we set the medium-term target for the total payout ratio* at around 50% of adjusted consolidated profit.

As shareholder returns based on our performance in fiscal 2017, we have chosen to pay an annual dividend of ¥110 per share, consisting of an interim dividend and a year-end dividend of ¥55 each, which will represent a year-on-year increase of ¥20 per share. In addition, we conducted share buybacks totaling ¥39.0 billion for the purpose of shareholder returns.

The total payout ratio was 50% of fiscal 2017’s adjusted consolidated profit.

As for fiscal 2018, we intend to raise dividend payments for the fifth consecutive year with a ¥20 increase over the level from fiscal 2017, making for an annual dividend of ¥130 per share, comprising an interim dividend and a year-end dividend of ¥65 each.

Going forward, we will continue to use internal reserves and capital gains generated from sales of cross-shareholdings to conduct promising growth investments in pursuit of rapid business growth. By allocating the additional profit generated through such growth to the enhancement of shareholder

returns, we will maximize shareholder value.

- The total payout ratio is an indicator of the weight of shareholder returns on the

profit of each period and is calculated using the following formula.

Total payout ratio = (total dividend payments + total share buybacks

(for shareholder returns) / adjusted consolidated profit

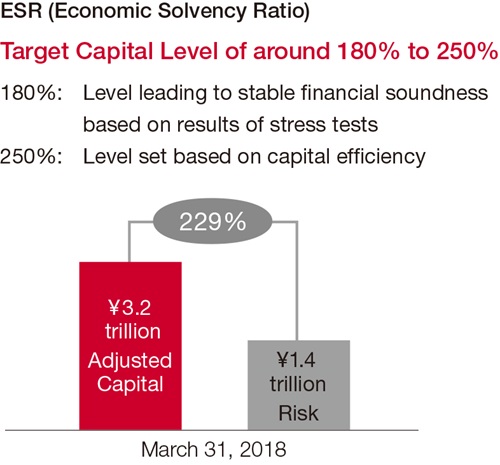

Maintenance of Financial Soundness

To maintain financial soundness, we manage capital based on the economic solvency ratio (ESR), determined by comparing economic value based on capital and risk.

Capital management is carried out by establishing a target capital level (ESR: around 180% to 250%) and a risk tolerance level as indicators of the amount of capital necessary for advancing Group strategies. When calculating ESR, we employ capital management methods based on the European Union’s Solvency II and other international capital regulations in order to increase global comparability, taking into account the recent disclosure status of insurance companies in Japan and overseas. Financial soundness is maintained and managed in this manner.

With an ESR of 229% as of March 31, 2018, the level is within our target capital range, indicating that we are maintaining robust financial soundness.

Improvement of Return on Risk

We use the return on risk indicator of ROR for making various management decisions in order to operate our businesses in a manner that ensures returns match or exceed the level of risks. By improving capital efficiency and maintaining financial soundness through increases in ROR, we seek to sustainably enhance corporate value.

When formulating business plans, the Group confirms the validity of plans in terms of the future outlook of the Group’s overall capital efficiency, financial soundness, and earnings stability as well as quantitative analyses of ROR of each business unit and line of business.

Not just limited to these areas, ROR functions as a yardstick for management in a wide area of individual policies. This indicator is thus utilized when selecting stocks as part of reducing cross-shareholdings, formulating natural catastrophe risk reinsurance strategies, making investment decisions regarding M&A activities, setting insurance product underwriting strategies and premiums, and evaluating officer and employee performance.